Why this rate cut matters (even if your lender doesn’t budge yet)

If you’ve got a mortgage, this moment could either save you thousands or cost you, depending on how you respond.

Let’s break it down.

What we’re seeing:

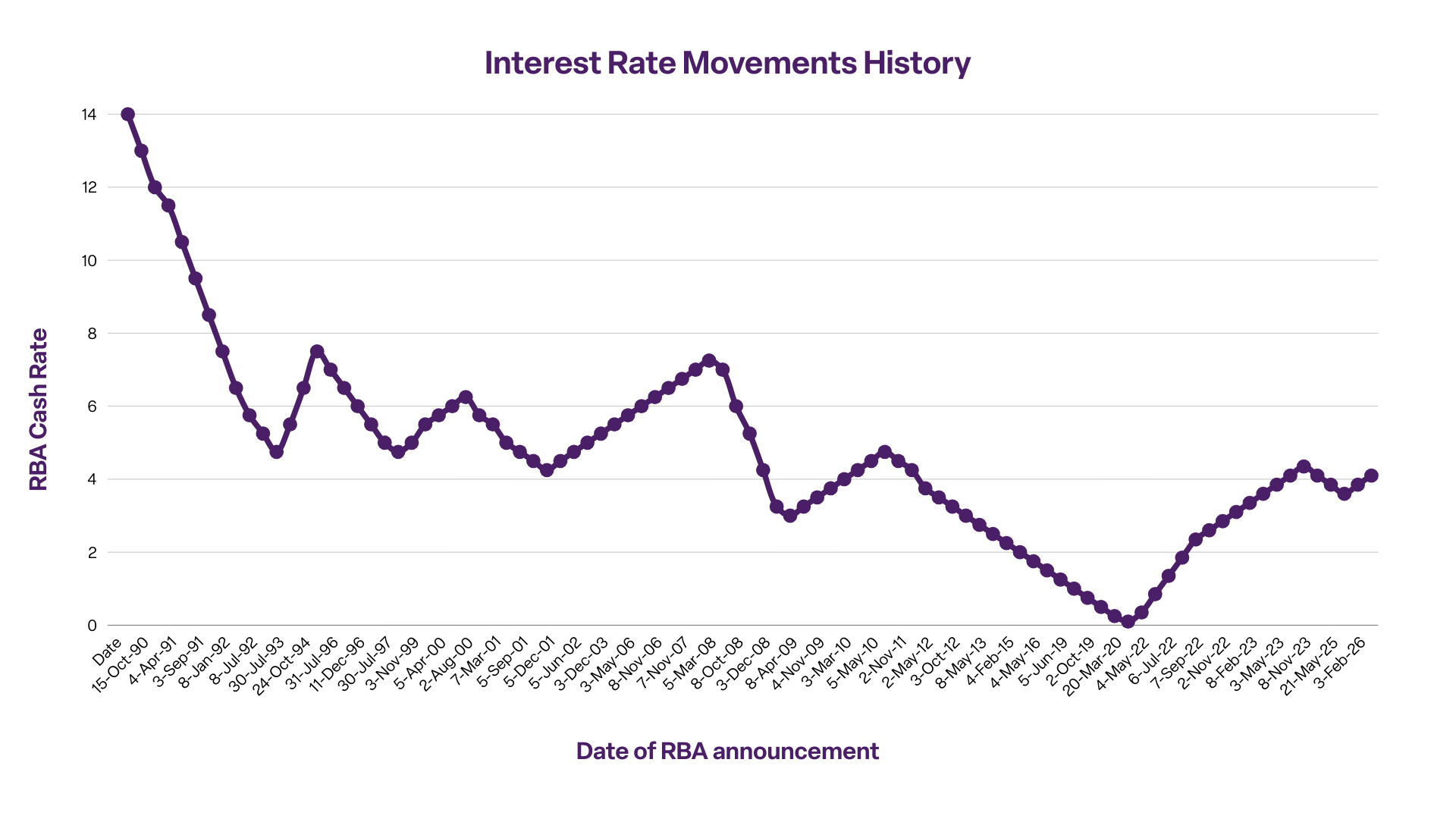

Many Aussie borrowers are still on rates around 6.15% p.a. based on ABS, RBA, and Lendi Group data.

That’s about $3,900/month in repayments on a $650,000 loan*

Meanwhile, some lenders on Aussie’s panel are now offering:

Variable rates from 5.8%-5.9%

Fixed rates as low as 5.29% p.a.

Even a 0.25% drop in your rate could save you up to $2,000–$3,000 per year. But if you keep your repayments the same, that’s where the real value lies. You could save over $100,000 in interest over your loan’s lifetime.**

Equity gains: Your home might be worth more than you think

Rate cuts aren’t the only thing working in your favour right now.

Home values in many parts of the country have nudged up over the past year, especially in Perth, Adelaide and Brisbane, unlocking usable equity for borrowers.

National example:

Detail | Amount |

Purchase Price (2024) | $790,000 |

Original Loan (80% LVR) | $632,000 |

Current Property Value | $810,000 |

Current Loan Balance | $653,000 |

Equity Gained | ~$20,000 |

Source: CoreLogic February 2025 Index and Lendi Group Rates based on our Generally Available Criteria.

That’s equity you could tap into for renovations, investments, or to negotiate better loan terms.

Don’t pay the loyalty tax

Let’s call it what it is: a loyalty tax. Some lenders offer their most desirable rates to new customers and leave loyal ones behind.

That’s why it’s so important to review your loan regularly. If your rate hasn't moved in the past year, or your lender hasn’t passed on recent cuts, you could be overpaying.

According to the RBA’s latest lending data, average variable rates for many borrowers remain above 6.1% p.a.

And that difference? It adds up fast.

What could you save?

Here’s a real-world comparison showing how refinancing a $650,000 variable home loan from 6.24% to 5.65% could save you over $100K and cut four years off your loan.

Loan Scenario | Before Refinance | After Refinance (Same Monthly Payment) |

Loan Amount | $650,000 | $650,000 |

Loan Term | 30 years | 30 years |

Interest Rate | 6.24% p.a. | 5.65% p.a. (Variable) |

Monthly Repayment | $3,998 | $3,752 |

Monthly Saving | $0 | $246/month |

Extra Monthly Repayment | $0 | $246 (voluntary, to match previous repayment) |

Total Repayments | $1,438,956 | $1,243,710 |

Total Interest Paid | $789,280 | $593,710 |

Interest Saved | $0 | $107,022 |

Years to Pay Off | 30 years | 26 years |

Years Saved | $0 | 4 years |

And it’s not just about monthly savings, it's about using this moment to future-proof your finances.

Will rates fall further in 2025?

Economists are still split. Some expect another rate cut later this year, especially if inflation continues to drop.

Others caution that the RBA may pause to assess how the economy absorbs these early cuts.

What we do know:

Wage growth is slowing

Retail spending is softening

Rent and energy costs remain high

Global volatility, especially trade-related, continues to pose risks

That’s why now is a smart time to lock in a better deal or review your strategy with an expert who knows the market.

Don’t miss the window: why timing matters

The May cut is your chance to reassess your home loan and take action. That might mean:

Refinancing to a sharper rate

Fixing your rate while they’re low

Using equity for renovations or debt consolidation

Shortening your loan term to reduce interest

Adding features like redraw or offset accounts

Even small changes now could mean major wins over time and the earlier you act, the more you can save.

Talk to an Aussie Broker today

Our brokers are here to help you navigate what this rate cut means for you. They’ll do the hard yards, comparing thousands of loans from over 25 lenders*** to help you get a better deal, faster.

We’ll review your current loan

Help you understand your equity position

Recommend options based on your goals