Home loan interest is usually calculated on your remaining balance, paying it down sooner may reduce long-term costs.

Even a small rate difference can change repayments and total interest over time. This matters because even a modest gap can cost more than borrowers expect.

The lowest advertised rate may not deliver the lowest total cost, once fees, features and fees are considered.

Reviewing your rate, refinancing, using an offset account or making extra repayments may help reduce interest. Borrowers may have several ways to improve loan costs.

Reviewing your home loan every 12 to 24 months can help you stay competitive. Existing borrowers do not always automatically move to more competitive pricing.

Home loan interest is one of the largest long-term costs in a mortgage, but is often overlooked when borrowers compare loans or review their current rate.

Over 20 to 30 years, even a small difference in interest rates can affect your repayments, cash flow and the total amount you pay back.

This guide explains how home loan interest works, what borrowers saw in 2025, and practical steps that may help reduce interest over time. It also looks at how rate type, loan features and regular reviews can affect the total cost of your loan.

Quick explainer: Common home loan terms

Before you compare home loan rates or look at refinancing, it helps to understand the terms that shape your interest costs and repayments.

Principal: Your principal is the amount you borrow from the lender.

Interest: Interest is the cost of borrowing. The lender charges it in addition to the amount you borrowed.

Repayment: A repayment is the amount you pay toward your home loan each repayment period. This is usually set up as either:

Principal and interest: You repay part of the loan balance as well as interest. Principal and interest repayments usually reduce the loan faster.

Interest only: You pay only the interest for a set period, so the principal does not reduce during that time. Interest-only repayments may be lower at first, but can increase the total interest paid over time.

Rate type: Your rate type determines how your interest rate is structured.

Understanding these basics makes it easier to compare home loans, assess whether your current rate is still competitive, and see where refinancing might reduce your interest costs.

You might also be interested in: Types of home loans

How does home loan interest work?

Home loan interest is usually calculated on your remaining loan balance.

So, the higher your balance, the more interest you are likely to pay. As your balance falls, your interest costs usually fall too. Your rate, repayment type, repayment frequency and loan term all shape what you pay over time.

Many home loans calculate interest daily based on your balance and charge it monthly, although methods vary by lender. In simple terms, the more you still owe, the more interest you are likely to be charged.

Remember, your interest rate is only part of the picture. The total interest paid over the life of a home loan can also be shaped by:

Your loan balance

Whether your repayments are principal and interest or interest only

How often you make repayments

Whether you make extra repayments

How long your loan term runs for

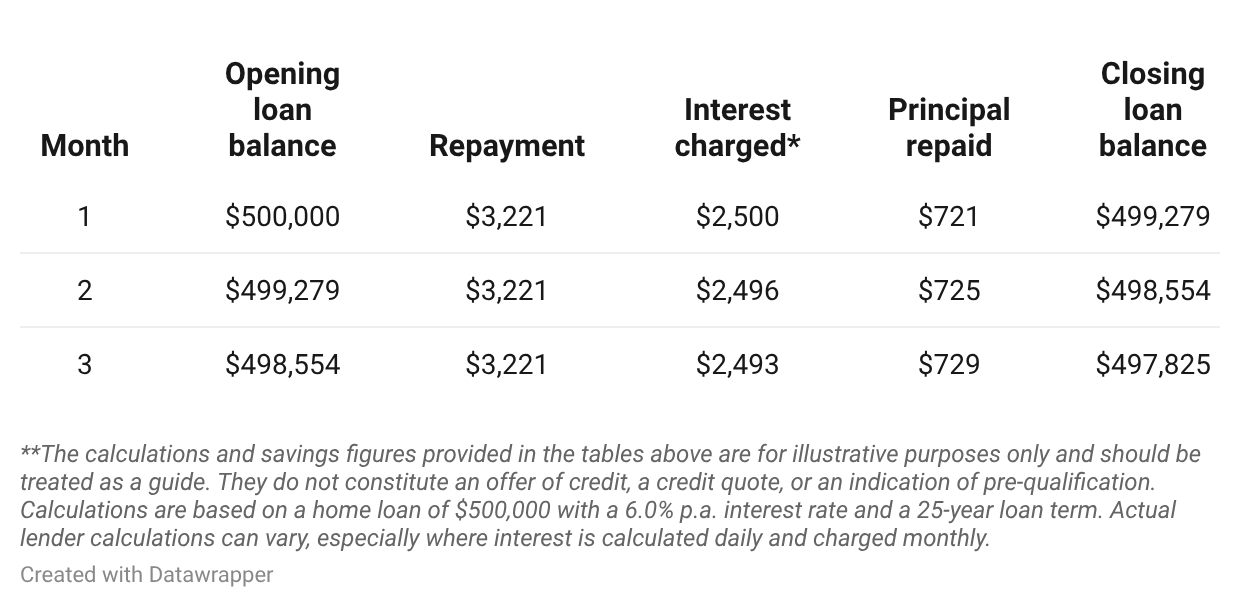

Even a small rate difference can affect both your regular repayments and long-term interest costs. At the start of a home loan, your balance is at its highest, meaning more of each principal and interest repayment goes towards interest, while less goes towards reducing the principal.

As the loan balance falls, more of each repayment goes toward paying down the loan. That is often why extra repayments made earlier in the loan can reduce interest costs more over time.

You might also be interested in: Extra repayments: How to pay off your home loan sooner

Here’s an illustrative example:

However, your interest rate may not remain the same throughout the loan term. Fixed rates usually apply for a set period. On the other hand, variable rates can change over time and may include features such as offset or redraw on some loans.

So when comparing the cost of a home loan over 20 to 30 years, it is important to look beyond one headline rate. The loan structure and the way you use its features can also make a difference.

What were home loan interest rates like in 2025, and why did they matter?

There was no single home loan rate for every borrower in 2025. Rates varied by lender, loan type, loan purpose and borrower profile.

But for many borrowers, home loan interest rates in 2025 were still well above the ultra-low settings seen in 2020 and 2021, which meant higher repayments and higher long-term interest costs than many households had become used to.

Why were rates still high compared to 2020–21?

The main reason was the RBA cash rate. After holding at 0.10% through much of 2020 and 2021, the cash rate rose sharply during the tightening cycle, then eased in 2025 before rising again in early 2026. The RBA cash rate table shows it moved to 4.10% in February 2025, 3.85% in May 2025 and 3.60% in August 2025, before increasing to 3.85% in February 2026 and 4.10% in March 2026.

Even with those 2025 cuts, borrowing costs remained well above pandemic-era lows.

You might also be interested in: RBA rate tracker: See the latest cash rate and what it means

What were many borrowers seeing in 2025?

A March 2025 Canstar snapshot of owner-occupier principal-and-interest loans showed average variable rates of 6.41% for basic loans, 6.99% for standard loans, 6.67% for package loans and 6.75% overall. The same snapshot showed average fixed rates ranging from 5.96% to 6.18% across one-year to five-year fixed terms. That helps explain why many borrowers still felt pressure in 2025, even after the first RBA cuts.

Loan purpose can also affect pricing. RBA housing lending rates data for February 2026 showed average rates on new owner-occupier loans at 5.72% compared with 5.90% for new investor loans. On outstanding loans, the average was 5.73% for owner-occupiers and 5.97% for investors. The gap varies by lender and product, but it is a useful reminder that investors often face different pricing.

Why were the 2025 rates crucial for borrowers?

For many households, 2025 was a year to reassess their loan. Borrowers who took out a mortgage, fixed their rate, or last reviewed their home loan during the ultra-low-rate period may have found their current rate no longer competitive.

With rates still materially higher than the 2020–21 era, checking the rate, fees and features on an existing loan became a practical way to see whether refinancing or renegotiating could reduce costs or improve fit.

What affects the rate you may actually get?

The rate available to you can depend on more than the headline rate on a lender’s website. Pricing may vary based on lender policy, loan-to-value ratio, whether the loan is owner-occupied or investment, and the loan features. Comparison rates, fees and product structure also matter when deciding whether a loan is competitive.

How much interest could you pay on your mortgage?

The total interest you pay depends on more than the loan size.

Your interest rate, loan term and repayment structure all affect both your regular repayment and the total cost over time.

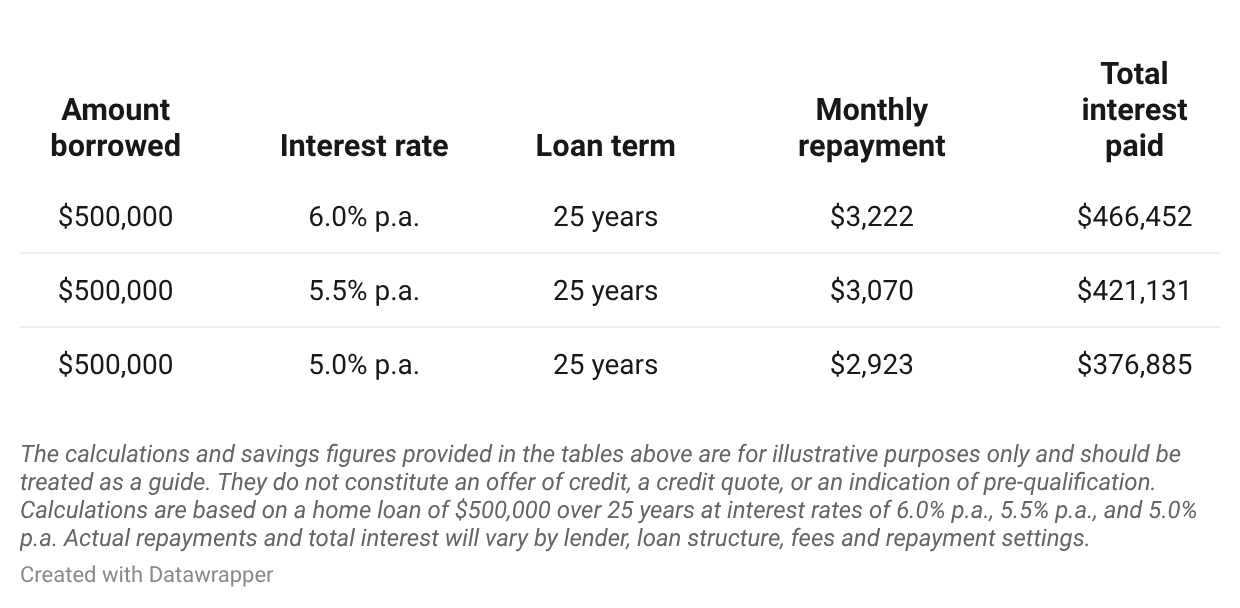

See our illustrative table below to see how a 0.5% rate difference could impact a $500,000 loan.*

On this example loan, the difference between 6.0% and 5.5% is about $151 a month and about $45,321 less in total interest over 25 years. Move from 6.0% to 5.0%, and the difference is about $299 a month and about $89,567 less in total interest over the same term. Highlighting why a rate review can matter, even when the gap looks small.

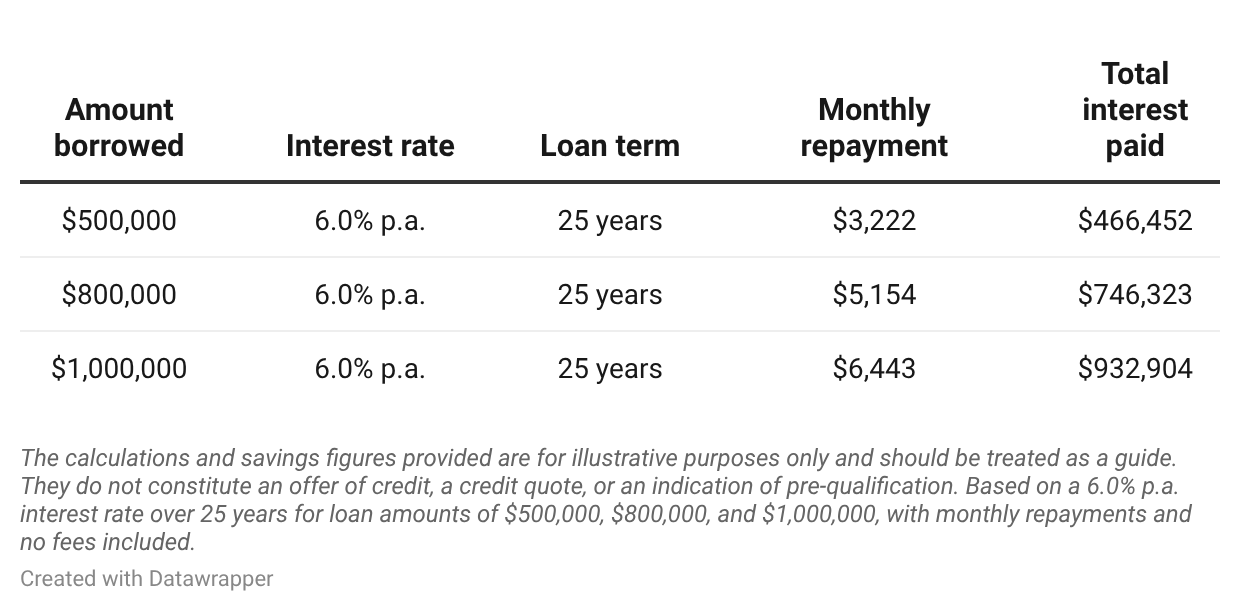

As the loan size rises, the dollar impact of your rate rises too. A larger balance means more interest can build over time, which is one reason bigger mortgages are often worth careful review.

Based on this example, if loan size increases from $500k to $1M, monthly repayment increases by about $3,222 and total interest by about $466,452.

What does this mean for borrowers?

A rate change does not just affect the number on your loan summary. It can change your monthly repayment, how much of your income goes towards the mortgage, how much interest you pay over the full term and how quickly you reduce the principal.

That does not mean every borrower should refinance. But it does mean reviewing your loan may be worthwhile if your current rate, features or structure no longer suit your needs. Moneysmart also notes there can be more than a 2% difference in variable home loan rates across the market, which is why comparing options can matter.

You might also be interested in: How home loan interest rate changes impact you

Fixed vs variable: How can your rate type affect total interest?

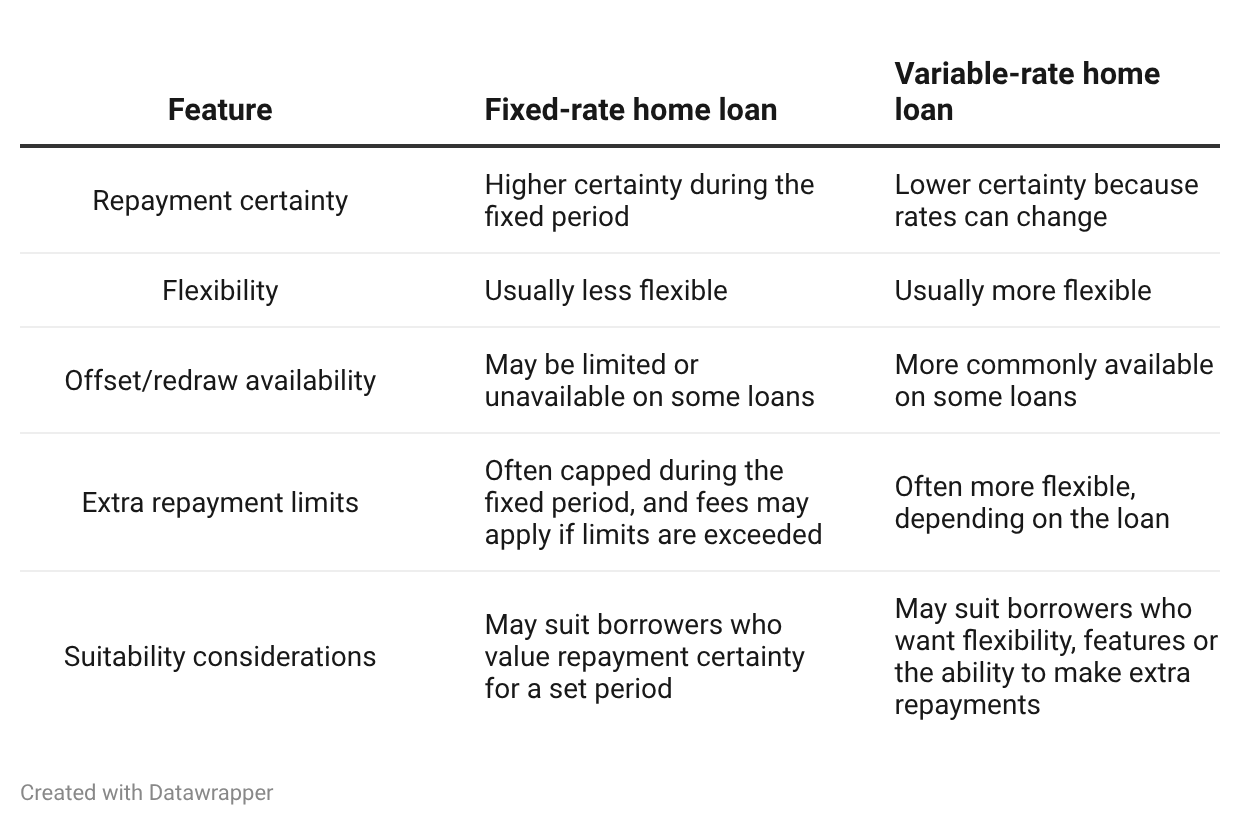

Your rate type affects more than your repayments from month to month. It can also affect how much interest you pay over time, which loan features you can use, and how much flexibility you have if your circumstances change.

A fixed rate locks in your interest rate for a set period, which can make repayments easier to predict during that time.

That may suit borrowers who want more certainty over short-term cash flow or prefer to know what their repayments will be for the fixed period. The trade-off is that fixed loans may limit features or cap extra repayments, with break costs or other fees applying in some cases.

On the other hand, a variable rate can fluctuate over time, so repayments can change. In return, variable loans often offer more flexibility. Depending on the loan, that may include an offset account, a redraw facility and more flexible extra repayments.

These features can matter because they may help some borrowers reduce interest, manage cash flow or pay down the loan sooner.

However, some fixed loans allow limited extra repayments. Some variable loans offer offset and redraw, while others do not. Some lower-rate products may also come with fewer features or tighter conditions, which is why it helps to compare the full loan structure, not just the headline rate.

The lowest advertised rate does not always produce the lowest total cost over time. Total interest can also be shaped by:

How rates change over the life of the loan

Whether the loan has ongoing fees

Which features are included

How much you keep in an offset account, if available

How long you stay on the loan

Takeaway: The better loan structure is not only about today’s rate. It is also about how you expect to use the loan.

What does this mean for borrowers?

A fixed rate may suit borrowers who want more repayment certainty for a set period. A variable rate may suit borrowers who value flexibility and features that may help reduce interest over time. For some borrowers, a split loan may also be worth considering, as it combines fixed and variable portions into a single loan.

The key is to compare the full picture: rate, fees, features, repayment flexibility and how you plan to use the loan.

You might also be interested in: Types of home loans in Australia: How to compare your options

How can you pay less home loan interest?

This section looks at practical ways to pay less home loan interest, from reviewing your rate to using loan features and repayments more effectively. Small changes can help reduce interest costs over time and improve how your loan works in your favour.

1. Ask your lender for a better rate.

Before refinancing, it can be worth asking your current lender for a rate review.

If you have had your loan for a while, your rate may no longer be as competitive as newer offers for similar borrowers.

Start by checking how your rate compares. Look at what your lender is currently advertising for similar loan types and borrower profiles. It also helps to compare your rate with other broadly similar loans in the market. Make sure the comparison is like-for-like, including:

Owner-occupier or investor

Principal and interest or interest only

Features such as offset or redraw

Package fees or ongoing fees

That gives you a stronger basis for checking whether your current rate is still competitive.

Then ask for a pricing review. Once you know how your loan compares, contact your lender and ask whether they can lower your rate. This can be a practical first step if you want to reduce interest costs without switching lenders. When reviewing your rate, lenders may consider:

Your repayment history

Your current loan balance

Your wider relationship with the lender

Current market competition

A lower rate is not guaranteed. But asking can help you work out whether your current loan is still competitive. Even a small rate cut may reduce your repayments and lower total interest over time.

If your lender cannot improve your pricing, that can also give you a clearer reason to compare refinancing options.

You might also be interested in: How can I negotiate with my lender to get a better rate?

2. Refinance your home loan.

Refinancing may be one way to reduce your interest costs , but it is not just about getting a lower rate. It is also a chance to check whether your current loan still suits your budget, repayment goals and the way you use the loan.

Review your loan regularly, not just once. It can make sense to review your home loan regularly, often every 12 to 24 months. It may also be worth reviewing sooner if:

Your lender has increased your rate

Your circumstances have changed

You want different loan features, such as an offset account

Your current loan no longer feels competitive

A regular review can help you check whether your loan is still competitive against what is available in the market.

Refinancing may also help you move to a more suitable loan. Depending on your eligibility and the costs involved, refinancing may help you access:

A lower interest rate

A loan with more suitable features

A different rate structure, such as fixed, variable or split

A loan that better matches your current financial position

The aim is to check whether your current loan still suits your needs, not just to switch lenders.

Look beyond the headline rate. A lower advertised rate can help, but it should not be the only factor in the decision. It is also worth comparing:

Comparison rate

Application or discharge fees

Ongoing fees

Offset or redraw features

Loan term and repayment type

These details can affect both the total cost of the loan and whether refinancing is worthwhile in practice.

Weigh the costs and potential savings. Refinancing can involve costs, and those costs need to be weighed against any potential interest savings. Depending on the loan, these may include discharge fees, application fees, valuation fees or government charges.

That is why refinancing works best as a full comparison exercise, not just a rate-chasing exercise. A more competitive rate can help, but the overall structure, features and costs matter too.

3. Use an offset account.

An offset account is a transaction or savings account linked to your home loan. The balance in the account is offset against your loan balance when interest is calculated, which may reduce the amount of interest charged.

How does an offset account work?

If your home loan balance is $500,000 and you keep $20,000 in an offset account, you may only be charged interest on $480,000. In general, the more money you keep in the account, the greater the potential interest savings.

Why can an offset account help?

An offset account can be useful if you keep regular savings or day-to-day cash in one place. Rather than putting that money directly into the loan, the balance may still help reduce interest while remaining available for everyday spending.

Check whether the loan includes an offset. Not all loans offer an offset account, and some only offer a partial offset. Availability can depend on the lender, loan product and rate structure, which is why it helps to compare the full loan package, not just whether an offset feature is included.

Compare the likely benefit with the cost. Some offset loans come with a higher interest rate or package fee. Whether an offset is worthwhile can depend on how much money you expect to keep in the account and whether the interest savings are likely to outweigh the extra cost.

For borrowers who keep only a small balance in the account, the feature may offer less value than it does for someone who holds larger savings there more consistently.

4. Make extra repayments.

Making extra repayments can help to reduce home loan interest over time. By paying more than the minimum required, you may reduce your loan balance faster, which can lower the interest charged and shorten the loan term.

If you reduce your balance sooner, you may pay less interest over the life of the loan. That means extra repayments may help you reduce total interest over time, pay off the loan sooner and build equity faster. Even smaller additional amounts can make a difference over a long loan term.

However, the benefit is not only the lower balance. Extra repayments may also reduce how long you stay in debt. Paying extra can mean:

More of your future repayments go towards principal sooner

Your loan term is shortened

Your long-term interest cost is lower than it would otherwise be

The actual effect will depend on your rate, repayment amount, loan balance and how early you start.

But remember, not all home loans treat extra repayments the same way. Variable loans often offer more flexibility, while fixed-rate loans may limit how much extra you can repay during the fixed period. Some fixed loans may also charge fees or break costs if you exceed the allowed extra repayment amount or repay the loan early.

That is why it is worth checking your loan terms before making larger additional repayments.

Use a strategy that fits your budget. Extra repayments can be effective, but they must remain manageable. A smaller, regular amount may be easier to maintain than a higher one. Borrowers may choose to make extra repayments by:

Increasing their regular repayment amount

Making one-off lump sum payments

Switching to fortnightly repayments, where suitable

The right approach will depend on your cash flow, loan type and broader financial priorities.

5. Avoid interest-only home loans.

If your goal is to reduce total interest over time, principal and interest repayments will often put you in a stronger position than interest-only repayments. That is because principal and interest repayments reduce the loan balance as you go. In contrast, interest-only repayments usually do not reduce the principal during the interest-only period.

With a principal-and-interest loan, each repayment goes toward the interest and reduces the loan balance. With an interest-only loan, repayments usually cover only the interest for a set period. The principal generally does not fall during that time.

If the balance is not paid down during the interest-only period, interest is usually charged on a higher amount for a longer period. That can mean slower equity growth, higher repayments later when principal repayments begin and higher total interest over the life of the loan. For borrowers focused on paying down debt sooner, that trade-off matters.

That does not mean interest-only loans are always the wrong choice. In some situations, they may suit borrowers with specific investment strategies or short-term cash flow needs, depending on their goals and circumstances.

But if the priority is reducing long-term interest and paying off the loan sooner, a principal-and-interest structure will often be more effective.

Check what happens when the interest-only period ends, as repayments can increase then. At that point, you usually start repaying both principal and interest over the remaining loan term, which can increase repayment pressure.

It helps to look beyond the lower initial repayment and consider the longer-term cost.

How often should you review your interest rate?

A home loan should be reviewed regularly rather than set and forgotten. Even if your repayments still feel manageable, it is worth checking whether your rate, features and loan structure are still competitive.

For many borrowers, reviewing their interest rate every 12 to 24 months is a sensible rule of thumb. It gives you a regular opportunity to check whether your current loan still suits your needs and whether similar borrowers can now access a more competitive rate or more suitable features.

It can also make sense to review your loan earlier, especially if:

The RBA cash rate has moved, and lenders have changed pricing

Your income, expenses or household situation has changed

You want different features, such as an offset account or more repayment flexibility

Your current loan no longer feels competitive

These changes can affect both what you are paying now and what may be available if you compare your options.

Lenders can also change pricing over time, and existing customers do not always automatically move to the most competitive rate. New customer offers, repricing decisions, product changes and shifts in lender strategy can all create a gap between what you are paying and what is available elsewhere. Which is why a regular review matters.

It helps you check whether your current rate is still competitive, rather than assuming it will remain competitive on its own.

A lower rate matters, but it is not the only thing to check. A proper review should also look at loan fees, offset or redraw features, repayment flexibility, fixed, variable or split rate structure and how the loan fits your current goals.

The right loan is not always the one with the lowest advertised rate. It is the one that best fits your circumstances overall.

Common mistakes borrowers make with home loan interest

Borrowers do not usually pay more interest because of one big mistake. More often, it comes from smaller decisions that go unchecked over time. Reviewing your loan regularly, understanding how your features work and checking whether your rate still suits your needs can all make a difference.

Ignoring rate rises or the end of a fixed rate.

A common mistake is ignoring your loan after a rate rise or when a fixed period ends. Both can change your repayments quickly and affect the competitiveness of your loan. If your fixed rate is about to expire, check the rate you will roll onto and whether it still suits your circumstances.

Not comparing rates regularly.

Another common issue is assuming your current rate will stay competitive on its own. Lenders can change pricing over time, and existing borrowers are not always automatically moved to the most competitive available rate. A simple review every 12 to 24 months can help you check whether your current loan is still competitive.

Leaving savings outside an offset when it’s available.

If your loan includes an offset account, keeping savings elsewhere may mean missing out on the chance to reduce the interest charged on your home loan. An offset may not suit every borrower, but if it’s available, using it well can help your savings work harder against your loan balance.

Making only minimum repayments.

Paying only the minimum is not always a problem. But if you could comfortably afford to pay more, it might mean paying more interest over time than necessary. Even smaller extra repayments may help reduce the principal sooner, which can lower total interest and shorten the loan term. The key is to make sure the strategy still fits your budget.

Focusing only on the headline rate.

A low rate can look attractive, but it does not always mean the loan is the better fit. Fees, offset access, redraw, repayment flexibility, and loan structure can all affect the overall value of the product.

Review your home loan interest regularly, not just once

Home loan interest is not just a background cost. It can shape your repayments, your cash flow and the total cost of owning a property over many years.

For many borrowers, paying less interest comes down to a few practical steps repeated over time: reviewing your rate regularly, comparing like-for-like loan options, using features such as offset well where suitable, and making extra repayments where your budget allows.

The right approach will depend on your circumstances, the lender's criteria, and the costs involved. However, a regular review can help you spot whether your current loan is still competitive.

An Aussie Broker can help you understand how your current loan works, compare it with other options, and check whether there may be a better fit for your needs.